21 May 2026

Why Architects’ Salaries Are So Low

and The Case for Taxing Extreme Wealth, Not Work.

Why wealth concentration is not a natural phenomenon, why the data may understate it, and whether a well-designed tax is necessary and achievable, by Floyd Slaski Architects Managing Director Hal Jones

Architects continue to occupy an elevated place in the public imagination. Saying “I’m an architect” still tends to attract a level of interest and respect that many professions do not. Yet financially, the profession has underperformed for decades compared with other traditional professional careers such as law and medicine. Why? With a shrug of the shoulders, we presume the reality of supply and demand, a lack of regulation of the function, and perhaps a creative zeal that adversely impacts our financial success.

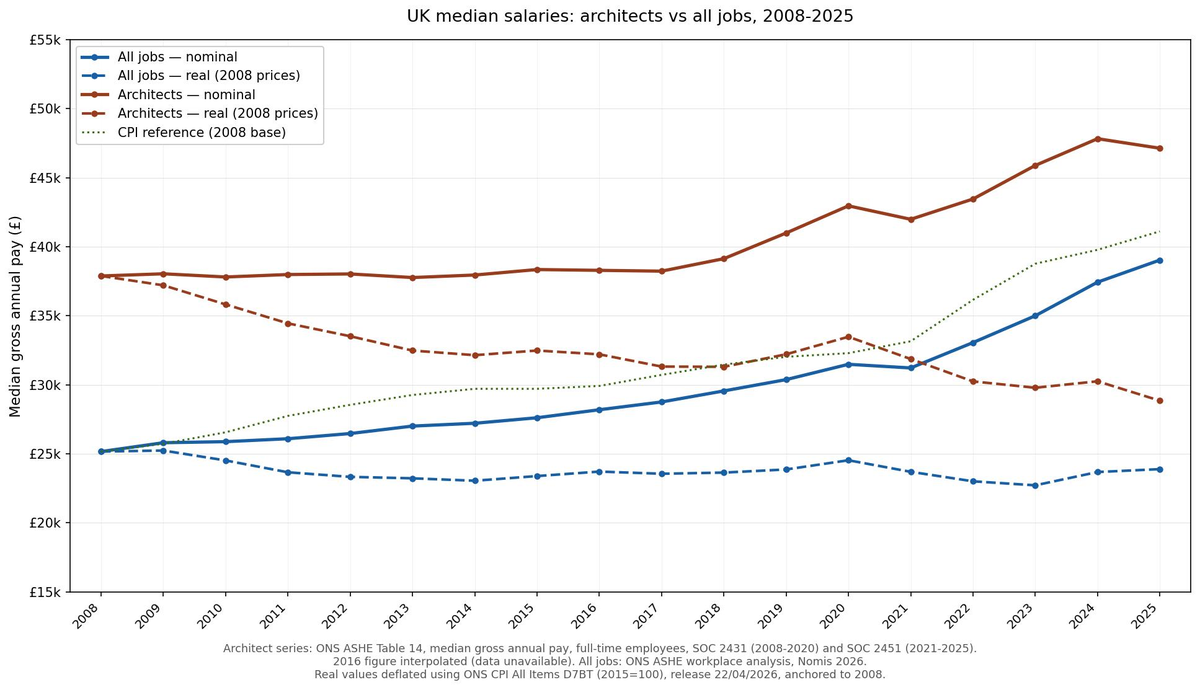

Architecture requires years of training, serious legal responsibility, and a challenging combination of creative, technical, contractual and people skills. Yet in real terms, already low median architect salaries have fallen significantly further since 2008.

According to ONS ASHE data, the median full-time architect salary was £37,887 in 2008. By 2025, in real terms adjusted to a 2008 base, that had fallen to approximately £28,851, a decline of nearly a quarter in purchasing power over seventeen years.1

At that level it becomes genuinely difficult to encourage young people into the profession with a clear conscience.

Figure 1: UK median salaries, architects vs all jobs, 2008-2025. Source: ONS ASHE. Real values deflated using ONS CPI D7BT. 2016 architect figure interpolated.

The obvious explanations, austerity, Brexit, Covid, are real but incomplete. The all-jobs median wage has also stagnated, with slight decline, in real terms over the same period. Architecture illustrates it with clarity, because the very asset that architects spend their careers designing, property, has done the opposite of their salaries. London house prices rose by approximately 70% in nominal terms between 2008 and 2023.2 Construction value has grown. Developer and landowner returns have in many periods been strong. The people who owned the assets did well. The people who did the skilled professional work of designing them did not.

That contradiction is the starting point for this article. Over the past four decades, western economies have increasingly rewarded ownership of assets, property, equities, financial instruments, rather than work. Wealth invested in assets compounds year on year. Wages, once spent on living costs, do not. When the return on capital consistently exceeds the rate at which the wider economy grows, an ever larger share of everything accrues to those who own assets, and an ever smaller share to those who sell their time and skill. The economist Thomas Piketty, in his landmark study of wealth and income across more than twenty countries, described this as the fundamental force of divergence in capitalist economies: when the rate of return on capital (r) exceeds the rate of economic growth (g), wealth concentrates.3 That condition, r greater than g, has been the dominant condition of western economies for most of the past forty years.

This article is not primarily about architects. But architects are a useful case study, because the profession sits precisely in the territory the argument is about: high skill, long training, real social value, but weak bargaining power against capital, and heavily exposed to the cycles of a property market whose gains flow predominantly to owners rather than to the people who design and build what makes those owners wealthy.

The Sunday Times Rich List offers one measure of the scale of the shift. The combined wealth of the UK’s thousand richest people stood at around £99 billion in 1997. By 2023 it had reached over £650 billion, a sixfold increase in nominal terms over twenty-six years, far outpacing both economic growth and wage growth over the same period. The 2026 edition of the Rich List, published in May 2026, recorded combined wealth of around £784 billion across the top 350 individuals and families — equivalent to roughly a quarter of UK GDP. Analysis by the Equality Trust, reported by the BBC in May 2026, found that the UK’s 157 billionaires now hold wealth equivalent to around 22% of GDP — a fivefold increase since 1989, when 15 billionaires held wealth equivalent to about 4% of GDP.4 This article is a summary of what that shift means, how it happened, and what a serious policy response might look like.

What this article is not arguing

Before proceeding, it is worth being clear. This is not an argument for:

● the abolition of markets or private ownership

● penalising entrepreneurship, innovation or financial success

● taxing the savings, pensions or homes of ordinary households

● treating all inequality as harmful or all wealth as illegitimate

● confiscating reasonable wealth that has been legitimately earned and already taxed

Rather, it is an argument that wealth compounding at the very top, at a scale where the annual return on assets exceeds what most people earn in a lifetime of work, requires democratic constraint if broadly shared prosperity is to be sustained.

Political landscape

During this period of stagnation and decline for the middle (including most architects) and the poor, political tensions have increased. Ongoing discussions and the rise of parties focussing on controlling immigration, especially illegal immigration, suggests there is a populist belief that immigration is somehow the cause, or a significant component, of our economic woes. In parallel there is an ongoing call for lower taxes, at a time when the state has national debt at its highest peacetime share of GDP for over half a century (around 95% of GDP in early 2026, compared with a post-WWII peak of roughly 250%) and insufficient wealth to adequately fund education, healthcare, the emergency services, defence and infrastructure.

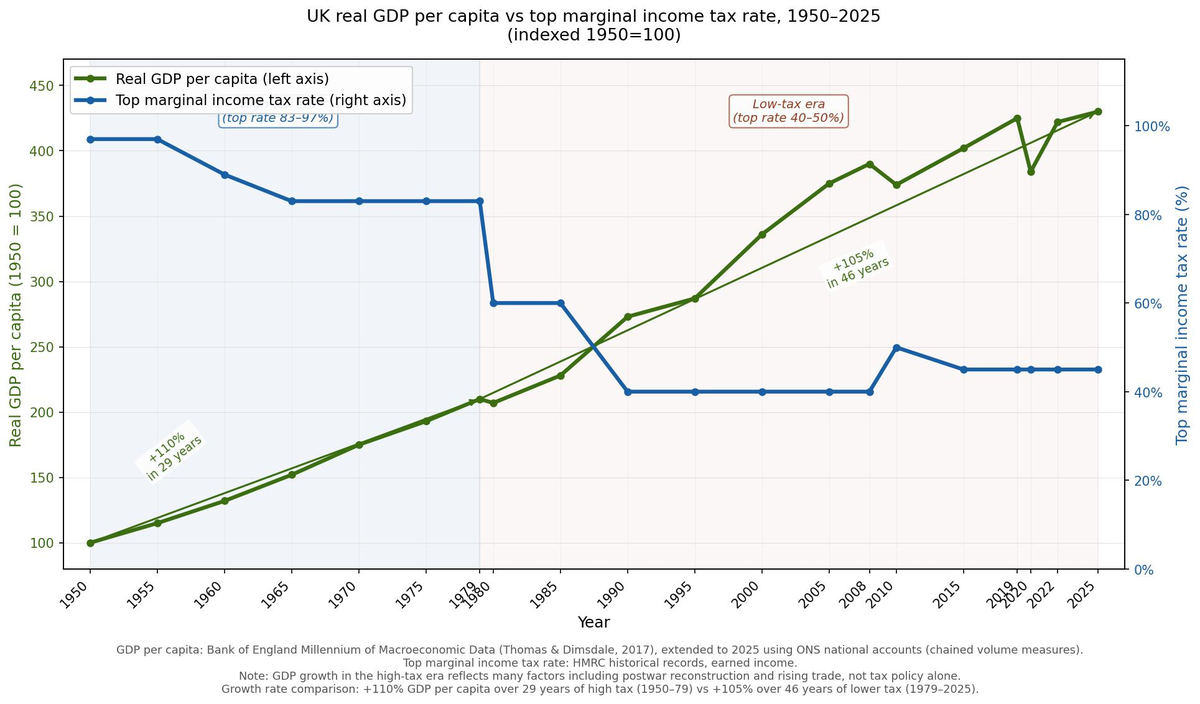

In this context why has taxation been demonised? Taxation is the friend of most people, protecting us from the super-rich hoarding wealth and enabling a healthy functioning society. Should we fear taxing the richest in society? In terms of income tax we can look historically at how the wealthiest have been taxed and compare this to growth:

Figure 2: UK real GDP per capita vs top marginal income tax rate, 1950-2025. Source: Bank of England Millennium of Macroeconomic Data (Thomas & Dimsdale, 2017), extended using ONS national accounts; HMRC.

The largely linear growth since 1950 continues regardless of the top tax rate. Naturally there were very different economic conditions throughout this period, but it does show that high top rate taxes are not necessarily a barrier to growth.

Tax wealth not work

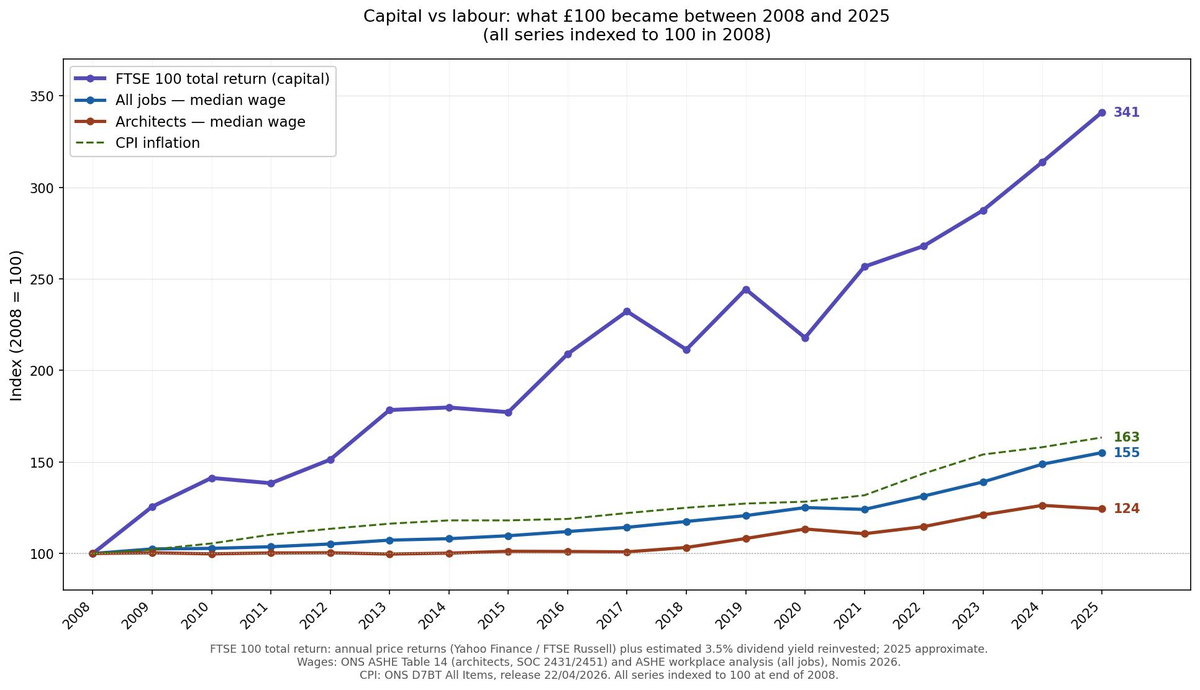

In recent years there have been growing calls for wealth taxes. It is a mathematical fact that the compounding wealth of the ultra-rich will continue to widen wealth inequality unless it is tackled. The graph below shows how wages (the reward for work) have in no way grown in proportion to stock market value.

Figure 3: Capital vs labour indexed to 100 in 2008. FTSE 100 total return calculated from annual price returns plus estimated 3.5% dividend yield reinvested; 2025 approximate. Wages: ONS ASHE. CPI: ONS D7BT, release 22/04/2025.

The graph shows what happened to £100 invested in the UK stock market in 2008 compared to £100 of wages over the same period. By 2025, the investment has become £341. The wages, once inflation is accounted for, have gone backwards.

But the gains shown in that purple line did not flow evenly across society. The median UK household has just £10,400 in savings and investments, enough to generate perhaps £500 a year in returns.5 For most people, the stock market’s performance over the past seventeen years is essentially irrelevant to their financial lives. The people who captured those gains are those with substantial financial assets to begin with, and that group is very small.

This article is not about the comfortably well-off: the successful professional with a good pension and a paid-off house. It is about a much smaller group whose wealth is large enough that capital returns alone, without working, without saving, without doing anything at all other than managing investments, exceed what most people earn in a year. For someone with £10 million in savings and investments, a modest 5% annual return produces £500,000 a year while the capital itself keeps growing. Work becomes optional and wealth becomes self-perpetuating. Because those returns compound year on year, the gap between that group and everyone else widens automatically. In other words, hard work is not rewarded. Assets are rewarded.

It is this dynamic, capital pulling away from labour and concentrating in fewer and fewer hands, that has pushed wealth taxation closer to the political agenda, and that underpins the arguments of economists like Gary Stevenson and Gabriel Zucman, whose work this article examines.

1. The problem: wealth is concentrating

Wealth inequality across western economies has reached levels not seen since the early twentieth century, and the official data almost certainly understates the true position. The share of total wealth held by the top one percent has risen sharply since the 1980s, while median household wealth and government net worth have stagnated or declined. This outcome is not an accident of market forces but the predictable consequence of removing the inheritance and wealth taxes that constrained concentration for three decades after the Second World War. Economists Gabriel Zucman, Arun Advani and Gary Stevenson argue that a well-designed minimum tax on extreme wealth is essential and is technically feasible. The principal remaining obstacles are political rather than economic:

● the underfunding of serious tax design work

● the structural alignment of the political class with the interests of the wealthy

● the systematic demonisation of the concept of taxing accumulated assets

Wealth taxes are not the only requirement for a healthy, functioning economy. Their omission is however an unnecessary contributor to our current economic decline. This topic should not be politically polarising. Accepting the unviability of having an ultra-rich class which is taking an increasing share of wealth away from governments, the middle and the poor, is surely a point of agreement, and the question should be: how do we collectively fix this?

In 1989, when the United States Federal Reserve began tracking the distribution of household wealth, the top one percent of households held approximately 24% of total national wealth. By the early 2020s that share had risen to 32%, roughly equal to the combined holdings of the bottom 90% of the population.6 The top ten percent, taken together, own approximately 90% of all equities.7 At the same time, the share of national income accruing to workers rather than to capital has fallen to near its lowest level in several decades.

These are American figures, but the UK, France, Germany, Australia and Japan have all experienced significant increases in wealth concentration over the same period. Research by Zucman and colleagues, drawing on harmonised data from the Netherlands, France, Italy, Brazil, Sweden and Norway, finds a consistent picture across every country studied: when all taxes are included at every level of government, the effective tax rate of billionaires is roughly half that of other social groups.8 France provides the starkest illustration. As Zucman has documented, if all French billionaires were to move to the Cayman Islands, their tax bill would be largely unchanged. France is, in effect, a tax haven for its own wealthiest citizens.

The mechanism driving concentration is not complex. Billionaire wealth has grown at an average real rate of 7.1% per year since 1987, against 3.2% for average wealth and 1.3% for average income per adult.9 This is the r > g dynamic Piketty identified operating in practice: capital compounding faster than the economy, necessarily taking a rising share of everything. The share of US wealth held by the 19 richest households has grown from approximately 0.85% at the height of the first Gilded Age, the era of Carnegie and Rockefeller, to approximately 1.8% today.10 By this measure, the current period is worse than the late nineteenth century, a fact that is not widely understood or discussed.

The pandemic years offered a stark illustration of this dynamic in compressed form. Between March 2020 and the end of 2021, as governments locked down economies and hundreds of millions of workers lost income or employment, global billionaire wealth increased by approximately $5 trillion, according to Oxfam’s analysis of Forbes data.11 In the UK, the collective wealth of the country’s billionaires rose by around a third over the same period. The objective of the quantitative easing that drove this was macroeconomic stabilisation rather than wealth transfer, but its distributional side effect was substantial asset price inflation that disproportionately benefited existing asset holders, while wages for workers in affected sectors fell or disappeared entirely.

2. The data understates the problem

A critical and insufficiently acknowledged point is that the official statistics on wealth inequality almost certainly understate the true position. Most wealth data comes from household surveys. The moderately wealthy tend to self-report reasonably accurately. The extremely wealthy do not, and in many cases are not required to.

The UK Wealth Tax Commission, an independent analysis led by economists Arun Advani and Andy Summers along with tax barrister Emma Chamberlain, found in 2020 that the most comprehensive UK household wealth survey is missing over £1 trillion in wealth held by the very richest households, and estimated that official figures understate true total UK household wealth by around 7%.12 Advani and colleagues have since demonstrated, using HMRC administrative data on the complete population of UK taxpayers, that investment income and capital gains are also systematically absent from official income statistics. When included, top income shares were rising during the austerity period even as official data suggested stability.13

At the extreme top of the distribution, the problem is more acute still. In France, on the eve of the abolition of the French wealth tax (legislated in late 2017 and taking effect from 1 January 2018), the declared taxable wealth of billionaires bore almost no relationship to their actual holdings. The effective wealth tax rate of French billionaires was 0.005%, not primarily because of offshore evasion, though that also occurred, but because the wealthiest were legally exempt from declaring most of what they owned.14 Zucman’s work demonstrates this pattern in every country where comparable research has been conducted.

When wealth is absorbed into the top 0.1%, it does not register in official data as increased inequality. It simply disappears from the data entirely, because billionaires do not complete surveys honestly and are frequently not required to declare their assets.

The implication for how inequality data should be interpreted is significant. When commentators point to surveys showing that the gap between, say, the 20th and 80th wealth percentiles has not widened substantially, that observation may be accurate within the range the survey can see. What it misses is the compression effect at the upper end: as wealth is extracted from the middle and concentrated at the very top, middle-class wealth shares appear to be declining relative to each other rather than to the billionaire class, which has largely vanished from the data.

This measurement problem has direct policy implications. Politicians and commentators who argue against wealth taxes frequently cite inequality data suggesting that concentration is not as severe as campaigners claim. The political class that benefits from the status quo is thereby provided with a permanent methodological alibi: the evidence does not show things are that bad, and the evidence does not show the tax would raise very much. Both statements are true of the evidence. Neither is reliably true of the underlying facts.

3. This was not inevitable: the historical record

The present distribution of wealth is sometimes framed as the natural outcome of markets rewarding talent and enterprise. The historical record does not support this framing. For approximately thirty years after the Second World War, the UK and United States maintained very high rates of both income tax and inheritance tax, with top marginal rates reaching around 90% in both countries.15 These taxes were imperfect instruments, but their structural effect was to prevent a class of people from emerging whose compounding wealth would outrun everything else, and to ensure that very large estates could not pass intact from generation to generation.

The result was not the stagnation that critics of high taxation predicted. It was the most sustained period of broadly shared prosperity in the modern history of either country. Real wages grew across the income distribution. Home ownership expanded. The foundations of a professional middle class, able to accumulate modest wealth through work and saving, were laid and maintained. This was not a naturally occurring state of affairs. It was a political achievement, dependent on specific fiscal structures, and it lasted as long as those structures remained in place.

Piketty’s historical analysis of wealth across Europe and the United States documents this pattern in detail. The high-tax postwar decades were not simply a period of good fortune; they were a period in which the structural forces driving wealth concentration were actively constrained by fiscal policy. His concept of patrimonial capitalism, an economy in which inherited wealth increasingly dominates over earned income, describes precisely the trajectory on which western economies have been set since the removal of those constraints.16 For architecture and similar professions, the implication is concrete: in a patrimonial economy, the returns to owning property systematically outpace the returns to designing it.

A particularly concrete illustration of what that erosion looks like in practice comes from inheritance data. The Resolution Foundation has documented that the total value of inheritances passed between generations in the UK has more than doubled in real terms over the past decade (from approximately £83bn in 2008-10 to approximately £189bn in 2018-20), and is increasingly concentrated at the top of the distribution: the wealthiest tenth of inheritors capture around half of all inherited wealth.17 For younger generations, research consistently shows that outcomes in terms of home ownership, pension provision and long-term financial security are now more strongly determined by parental wealth than by individual earnings or effort.18

When those rates were cut in the early 1980s under Reagan and Thatcher, the constraint was removed. Tax policy was a major enabling condition of the subsequent concentration, though not the only one: technological change, globalisation, the rise of superstar firms and the financialisation of western economies all contributed. The post-war period of broad middle-class prosperity was not the default condition of market economies. It was an exception, maintained by deliberate policy, and its erosion since the 1980s is the consequence of removing that policy.

4. Why the current tax system fails

A common assumption is that progressive income tax performs the function of constraining wealth concentration at the top. The empirical evidence across multiple countries shows clearly that it does not.

When you are sufficiently wealthy, it is legally straightforward to arrange your affairs so that your wealth generates almost no taxable income. The primary mechanism is the ownership of large companies. A billionaire who controls a major corporation can instruct it not to pay dividends and can avoid realising capital gains by refraining from selling shares. If they need money for expenditure, they borrow against their shareholding. Loans are not income. The shareholding appreciates year after year without any taxable event occurring, and when the billionaire eventually dies, the cost base of the assets resets to their value at the date of death, meaning that an entire lifetime of capital appreciation passes untaxed. ProPublica’s investigation into US billionaires’ tax records found that two filing years (2007 and 2011) Jeff Bezos paid no federal income tax, and in 2011 also claimed a $4,000 child tax credit.19 This involved no illegality. It was the straightforward consequence of structuring wealth to prevent income recognition.

In Europe, an additional mechanism is widespread. Most European billionaires hold their shares through intermediate holding companies rather than directly. When a business pays dividends upward to the holding company, those payments are treated as inter-company transfers rather than income to an individual, and the personal income tax never applies. Zucman notes a historical parallel: in May 1933, JP Morgan Jr testified before the US Senate Banking and Currency Committee (the Pecora Commission) that he and many of his partners had paid no income tax in 1930, 1931 or 1932 — a disclosure that contributed directly to the 1934 introduction of US anti-avoidance rules on personal holding companies.20 Most of Europe never introduced the anti-avoidance rules that made this harder in the American context, which is why effective personal income tax rates fall to near zero for billionaires in France, the Netherlands and comparable countries.

These mechanisms, dividend suppression, asset-backed borrowing, holding company structures, operate specifically at the scale of extreme wealth. They are not available to people with ordinary savings, pensions or investment portfolios.

UK-specific research from Advani, Hughson and Summers, using anonymised HMRC administrative data on the complete UK taxpayer population, confirms the same pattern domestically. Effective tax rates fall sharply at the very top of the income and capital gains distribution, with a quarter of those in the top 1% paying effective rates at least 9 percentage points below the headline rate.21 Their calculation is that if all individuals with income above £100,000 simply paid the headline rates they are nominally subject to, an additional £23 billion per year would be raised.

The progressive income tax system, for all its historical importance, simply does not reach billionaires. They remain, in any meaningful sense, outside the realm of individual income taxation.

5. The standard objections

5.1 Wealth taxes have failed before

The most frequently cited empirical argument against wealth taxes is that most countries that introduced them subsequently abandoned them: of the twelve OECD countries that levied an individual net wealth tax in 1990, only four still did by 2017 (Norway, Spain, Switzerland and France, with France abolishing its tax in 2018).22

Closer examination reveals, however, that those failures shared consistent design defects rather than demonstrating any inherent impossibility. Zucman’s analysis of France is instructive. The wealth tax abolished from 1 January 2018 (legislation passed in late 2017) started at a threshold of one million euros and included extensive exemptions: a billionaire who owned more than 25% of a large company paid no wealth tax on that stake at all. The effective rate for billionaires was 0.005%, not because of evasion but because the wealthiest were legally excluded from the tax base.

The 2020 UK Wealth Tax Commission concluded that an annual wealth tax would face serious challenges around the valuation of illiquid assets and that avoidance responses could erode 7-17% of the tax base at a 1% rate. On those grounds it recommended against an annual wealth tax and set out a detailed proposal for a one-off wealth tax (capital levy), alongside reforms to existing capital taxes.23

Zucman’s response rests on a fundamental redesign. His proposal starts at a high threshold, $100 million or more, with no exemptions at all. The high threshold dramatically reduces the administrative burden. The no-exemption rule prevents the carve-outs that hollowed out every previous attempt. The liquidity problem is addressed by allowing payment in shares.

Just because something is difficult does not mean that it is not possible nor that is it is not worth achieving. Take all the incredible advances humans have made, all of them overcoming difficulties that to previous generations seemed unthinkable. Thriving human societies with effective wealth distribution are a benefit to everyone and are worth fighting for.

5.2 The wealthy will simply leave

The capital flight objection is the argument that receives the most political attention. Research on the Swedish wealth tax repeal in 2007 found that the repeal reduced the propensity of wealthy individuals to leave Sweden by 30%.24

More recent evidence is reassuring , though it does not suggest that the behavioural response is zero. HMRC data reported by the Financial Times in August 2025 showed that the number of non-doms leaving the UK following the reform of non-domicile taxation was in line with or slightly above official forecasts; consultancy analysis by Chamberlain Walker (December 2025) put the figure at around 1,800 departures in 2024/25, against the OBR’s forecast of 1,200. Some high-profile billionaires, including Lakshmi Mittal and John Fredriksen, have relocated to lower-tax jurisdictions. The most rigorous recent study, Advani, Burgherr and Summers (LSE/Warwick, May 2025), finds that the 2018 reform of UK non-dom taxation caused around 4.9% of those affected to leave; a real but contained response, while net tax revenue still rose by approximately £311 million in 2020 because those who stayed paid substantially more.25 The dramatic figures of 16,500 millionaires leaving in 2025 came primarily from Henley and Partners, a relocation consultancy with an obvious commercial interest in promoting high emigration narratives, and were systematically debunked by the Tax Justice Network. An LSE study found that the large majority of Britain’s wealthiest people would not leave for tax reasons.26

It must be acknowledged, however, that designing a wealth tax that works in a single country is genuinely harder than designing one across many. The 2021 global corporate tax agreement took years of international negotiation and the personal wealth equivalent would be more difficult still: most non-G20 jurisdictions actively compete for high-net-worth migrants through golden visas, low-tax regimes and (in the UAE and parts of the EU) bespoke non-dom packages. A unilateral wealth tax that fails to coordinate with comparable jurisdictions will lose more of its base to migration than a coordinated one. More fundamentally, the capital flight argument is a design problem with known solutions. Zucman’s central insight is that the appropriate tax base is the location of the assets rather than the residence of their owner. He proposes conditioning market access on meeting the minimum tax standard, in the same way as companies from non-participating jurisdictions are treated under the 2021 global minimum corporate tax agreed by 136 countries.27

5.3 It would not raise enough money to justify the disruption

A common objection, often framed as pragmatic rather than ideological, is that even a well-designed wealth tax would raise too little revenue to justify the administrative complexity and political controversy involved. Modern states spend hundreds of billions annually. What difference would a few extra billions make?

The arithmetic does not support the premise. Zucman's G20 proposal estimates $200-250 billion annually at the global level from a 2% minimum tax on billionaire wealth. In UK terms, cautious estimates imply revenues in the tens of billions rather than the single billions critics tend to imply. The Wealth Tax Commission estimated that a one-off levy at modest rates could raise around £260 billion over five years (a 1% annual tax on wealth above £500,000, paid over five years). Advani, Hughson and Summers calculate that simply ensuring high-income individuals paid the headline rates nominally applicable to them would raise an additional £23 billion per year. Such figures are comparable to the annual budgets of major government departments.

But the more important point is that revenue is not the only purpose. A modest annual wealth tax operates partly as a fiscal instrument and partly as a structural counterweight to compounding concentration. If wealth at the top grows indefinitely faster than wages and economic growth, even a government with balanced books becomes progressively weaker relative to private concentrations of capital. Slowing that process has value independently of what it raises.

The argument also sits awkwardly alongside the institutional effort devoted over recent decades to reducing taxes on capital, maintaining inheritance tax reliefs, designing non-dom regimes, and policing benefit fraud worth a fraction of the sums involved. States routinely commit large resources to relatively modest fiscal questions when the political priority exists. The claim that taxing extreme wealth is uniquely impractical tends to reflect political reluctance rather than administrative reality.

5.4 Double taxation

A more philosophical objection holds that taxing accumulated wealth amounts to taxing the same money twice. This argument does not survive scrutiny as a general principle. Income taxes, council taxes, stamp duties and VAT all represent successive rounds of taxation on the same underlying economic activity. The principle that assets, once acquired, should be permanently exempt from further taxation is not a general rule of any tax system; it is a specific exemption carved out over time.

The argument collapses entirely in the context of inherited wealth, where the current holder paid no tax on their acquisition. It is worth noting also that the middle class already pays an effective annual wealth tax in the form of council tax and property taxes, typically at rates representing 1% or more of the asset value.28 The argument that a comparable charge on the holdings of billionaires would be confiscatory sits awkwardly alongside untroubled acceptance of similar rates applied to the primary asset of working families.

5.5 High taxes stifle innovation and productive investment

A fourth objection, is that concentrated wealth enables the investment, risk-taking and innovation that drives economic progress.

The first point is that it distinguishes very poorly between different types of wealth. The founder who risks capital to build a business and the heir who inherits a diversified investment portfolio are both described as wealthy, but their economic functions are entirely different. A policy, such as the Zucman 2% minimum tax on net wealth above $100 million with no exemptions, would affect the passive investor far more than the active entrepreneur, because the active entrepreneur’s wealth is typically illiquid and concentrated in a single business.

The second point is empirical. The postwar decades, when top marginal tax rates reached 90% in both the UK and the United States, were not a period of economic stagnation or innovation drought. They produced the NHS, the interstate highway system, the space programme, the foundation of Silicon Valley and the most sustained period of broadly shared economic growth in modern history.

The third point is that the proposal specifically targets passive compounding rather than productive enterprise. A 2% annual minimum tax on net wealth above $100 million leaves billionaire wealth growing at roughly 5% annually, still far exceeding GDP growth. It simply ensures that wealth at a scale where it has permanently escaped income taxation contributes something to the societies whose legal systems, infrastructure and educated workforces made that wealth possible.

6. What a well-designed tax would look like

Zucman’s proposal, developed for the G20 under the Brazilian presidency in 2024 and now under active debate in France, Belgium, Spain and elsewhere, offers the clearest technical model currently available.29 The caricature of a wealth tax as a blunt confiscatory instrument bears little resemblance to what is actually proposed.

The core idea is a minimum tax expressed as a fraction of wealth rather than of income. Income cannot serve as the base for taxing the super-rich: they can legally structure their affairs so that reportable income is close to zero regardless of how progressive the nominal schedule is. A minimum expressed as a fraction of wealth bypasses all of the avoidance mechanisms built around income recognition.

The proposed rate is 2% of net wealth, applying in its baseline form to the world’s approximately 3,000 dollar billionaires; an extended variant would apply to centi-millionaires (those with more than $100 million). Given that billionaire wealth has grown at a real rate of 7.1% per year since 1987, a 2% minimum tax would leave it growing at roughly 5% annually, still far faster than average wealth or income. The G20 report estimates $200-250 billion annually at the global level.30 Polling consistently shows 70-80% public support across every country where it has been tested, including the UK, where a 2025 Survation poll for Patriotic Millionaires UK found 80% of UK millionaires in favour of a 2% tax on wealth over £10 million.31

In a UK political context, two current proposals are worth comparing to the Zucman baseline. The Green Party’s 2024 general election manifesto proposed a 1% annual wealth tax on net wealth above £10 million and 2% on net wealth above £1 billion, projecting additional revenue of £50–70 billion per year by the end of the next Parliament. This is closer in design to Zucman’s extended (centi-millionaire) variant than to the billionaire-only baseline, and is more aggressive at the very top. Separately, Wes Streeting MP, following his resignation from cabinet in 2026 and ahead of a Labour leadership bid, set out a different proposal: equalising capital gains tax rates with income tax (20/40/45%), with carve-outs for genuine entrepreneurs, and closing the loopholes used to convert work income into capital gains. Streeting cited Centre for the Analysis of Taxation (CenTax) modelling estimating revenue of up to £12 billion per year. Strictly this is a capital gains reform rather than an annual wealth tax, but its underlying logic that asset-based income should not be taxed more lightly than earned income, is the same as the Zucman case for a minimum effective rate.

A 2% minimum tax would not reduce wealth concentration and would not even stabilise it. It would simply ensure that billionaires are no longer the one group in developed economies structurally guaranteed to pay lower effective tax rates than everyone else.

7. The democratic argument

Beyond the fiscal arithmetic, there is a democratic case for wealth taxation that tends to be crowded out by the technical debate. Wealth is power. An extreme concentration of wealth means an extreme concentration of the power to shape political outcomes: to fund political parties, to own media, to sustain well-resourced lobbying operations, and to exercise influence over the regulatory environment in which businesses operate.

The evidence for this influence is concrete. In the United States, the 2010 Citizens United ruling removed limits on political spending by corporations and wealthy individuals; in the 2020 election cycle, the top 100 donors contributed around $1.6 billion to political campaigns.32 In the UK, the ten largest donors to political parties between 2001 and 2020 collectively gave over £100 million, the large majority to parties that subsequently cut taxes on income and capital.33 In France, billionaires own approximately 80% of private media by circulation.34 The lobbying industry in the US alone spends over $4 billion annually, with financial services, real estate and energy consistently among the largest spenders.35

Plato identified the tension between extreme wealth and democratic self-government more than two thousand years ago. The progressive tax structures of the twentieth century were, in part, a conscious institutional response to that tension. Their dismantling has been followed by a drift back toward the conditions they were designed to prevent, and the political turbulence of the past decade, the collapse of established political coalitions, the rise of anti-system parties of both left and right, the erosion of institutional trust, is at least partially explicable as a consequence of governing institutions perceived as more responsive to the interests of a very small minority than to those of the population as a whole.

8. The structural problem of political implementation

Perhaps the most important and least discussed obstacle to wealth taxation is not technical but structural: the people who would design and implement a wealth tax are, in both the UK and the United States, predominantly drawn from the social cohort that would be most affected by it, or are financially dependent on that cohort in ways that create persistent conflicts of interest.

The revolving door between senior political roles and well-paid positions in finance, consultancy and private equity is not an occasional feature of British political life but the normal trajectory of a successful career at the top of politics. David Cameron is reported to have earned around $10 million (roughly £7 million) from advisory and share-related work for Greensill Capital between August 2018 and the company’s collapse in March 2021, through routes that depended on the networks his time in office had generated.36 The pattern extends beyond any single party. Senior politicians across the political spectrum routinely transition into financial services, advisory roles and corporate directorships whose value derives from their political connections.

The consequence for wealth tax design is predictable and has been consistently observed. The result is characteristically legislation that reads as a wealth tax in its public presentation but contains provisions that render it ineffective at the top of the distribution. The UK stamp duty surcharge on additional residential properties provides a small but telling illustration: the legislation interacts with a pre-existing rule (Finance Act 2003, section 116(7)) under which purchases of six or more dwellings in a single transaction are treated as non-residential and so escape the surcharge — an interaction that served no articulated policy rationale but happened to exempt the largest portfolio investors from the charge applicable to everyone else.37

Gary Stevenson, who spent a decade attempting to engage the political process on these questions before concluding that direct public communication was more productive than lobbying, is frank about his prognosis. He believes the political will to introduce some form of wealth taxation will eventually arrive, if public pressure makes it unavoidable. However, he also believes the implementation will probably be compromised, producing a headline announcement, a loophole-riddled bill, and a subsequent failure that becomes further evidence that wealth taxes cannot work. His response is to build public understanding deep enough that people can recognise the loopholes when they appear and sustain pressure for them to be closed.

9. What should happen

The most important immediate step is the funding of serious technical design work. The 2020 Wealth Tax Commission demonstrated that a relatively small investment in rigorous, interdisciplinary analysis can produce a credible and detailed blueprint. That work has not been extended into a sustained government programme.

The right design for a UK minimum wealth tax could follow the Zucman baseline and start at the equivalent of $100 million (around £80 million) in net wealth, with no exemptions. Once the valuation, reporting and enforcement mechanisms are in place and demonstrably working at that level, the threshold could be lowered in subsequent stages — say to £20 million — to capture a wider range of very large estates while preserving the design discipline that made the higher-threshold version administrable. It would include all asset classes without exemption. It would incorporate exit charges that continue to apply for a substantial period after emigration. And it would include extraterritorial provisions under which income derived from UK assets remains taxable regardless of the owner’s place of residence.

This design would sit alongside, and require, complementary reforms. Inheritance taxation requires structural reform: the proliferation of reliefs and exemptions has reduced the effective rate paid on large estates to a small fraction of the statutory 40%, and the step-up in basis rule in the USA allows entire lifetimes of capital appreciation to pass untaxed at death.38 Similar avoidance mechanisms exist in the UK. Enforcement capability requires sustained investment. Capital gains tax reform, particularly the equalisation of rates between capital income and employment income, would address a structural distortion that currently privileges the returns of owners over the earnings of workers.

None of this requires a departure from established principles of taxation. It requires the political will to apply those principles to the segment of the population to which they currently do not, in practice, apply.

10. Conclusion

The arithmetic of this problem is simple, but the politics are not. Wealth compounding at 7% annually in economies growing at 2% will, in the absence of effective taxation, continue to concentrate. The people who own that wealth will own a rising share of everything, and everyone else, working families, professional households, and governments, will own correspondingly less. This is not a prediction based on contested assumptions. It is what has been happening, measurably and consistently, for four decades.

For architects specifically, the trajectory is visible in the numbers we started with. The profession designs buildings whose value has grown enormously. The wealth generated by that value has accumulated to owners of land and capital, not to the people who did the skilled work of design. That is a microcosm of a pattern playing out across the professional middle class in every western economy. It is not the result of architects, or teachers, or engineers, or accountants working less hard or less well than previous generations. It is the result of an economy that has progressively tilted the rules in favour of owning assets over earning income, and has done so through specific and reversible policy choices.

The history of the post-war period shows clearly that the outcome is not predetermined. The taxes that constrained concentration were imperfect but effective. Their removal was a political choice made in specific ideological conditions, not an economic inevitability. The case for restoring something equivalent rests not on ideology but on arithmetic: if you do not want extreme wealth concentration to continue, you have to tax it at rates sufficient to offset the compounding effect. The question worth debating seriously is how to design the tax so that it achieves this without the avoidance failures that undermined previous attempts. That question has technically credible answers, as Zucman’s work demonstrates.

Those conditions will not be created by the political class whose structural interests are described in section 8. They will be created, if they are created, by public understanding of the connection between extreme wealth accumulation and declining living standards running deep enough to sustain pressure not just for the headline announcement but for the quality of implementation that makes the announcement mean something.

References

1. ONS Annual Survey of Hours and Earnings (ASHE), Table 14, median gross annual pay, full-time employees, SOC 2431 (2008-2020) and SOC 2451 (2021-2025). Real terms calculated using ONS CPI All Items index D7BT, release 22 April 2025.

2. ONS/HMLR UK House Price Index, monthly series, annual averages 2008-2023.

3. Thomas Piketty, Capital in the Twenty-First Century, Harvard University Press, 2014.

4. Sunday Times Rich List, 1997 and 2023 editions.

5. ONS Wealth and Assets Survey, Wave 7 (2018-2020), Table 6.2, median net financial wealth by household.

6. Federal Reserve Distributional Financial Accounts, Series DFA, Q3 2023.

7. Edward Wolff, A Century of Wealth in America, Belknap Press, 2017, updated with Federal Reserve data.

8. Gabriel Zucman, A Blueprint for a Coordinated Minimum Effective Taxation Standard for Ultra-High Net Worth Individuals, G20 Report, June 2024. Available at gabriel-zucman.eu.

9. Ibid.

10. Ibid.; see also Emmanuel Saez and Gabriel Zucman, The Triumph of Injustice, Norton, 2019.

11. Oxfam, Inequality Kills, January 2022, based on Forbes Billionaires List data.

12. Arun Advani, Emma Chamberlain and Andy Summers, A Wealth Tax for the UK, Wealth Tax Commission Final Report, December 2020. Available at ukwealth.tax.

13. Arun Advani, Jake Ooms and Andy Summers, Missing incomes in the UK, Journal of Social Policy, 53(2), 2024, pp. 386-406.

14. Zucman, G20 Report, 2024 (see reference 8).

15. HMRC, Historical rates of Income Tax; IRS Historical Statistics.

16. Piketty, Capital in the Twenty-First Century, Part Four.

17. Resolution Foundation, Intergenerational Audit for the UK, 2023.

18. Ibid.; see also Institute for Fiscal Studies, Intergenerational Transfers, 2021.

19. Jesse Eisinger, Jeff Ernsthausen and Paul Kiel, The Secret IRS Files, ProPublica, 8 June 2021.

20. Zucman, G20 Report, 2024 (see reference 8).

21. Arun Advani, Helen Hughson and Andy Summers, How much tax do the rich really pay?, Oxford Review of Economic Policy, 39(3), 2023, pp. 406-437.

22. Zucman, G20 Report, 2024 (see reference 8).

23. Advani, Chamberlain and Summers, Wealth Tax Commission Final Report, 2020 (see reference 12).

24. Katrine Jakobsen, Henrik Kleven, Jonas Kolsrud, Camille Landais and Mathilde Muñoz, Taxing Top Wealth: Migration Responses and their Aggregate Economic Implications, NBER Working Paper No. 32153, February 2024.

25. Financial Times, Non-dom exodus smaller than feared, HMRC data shows, August 2025.

26. Arun Advani, David Burgherr and Andy Summers, ‘Taxation and Migration by the Super-Rich’, LSE/CenTax/Warwick CAGE working paper, 6 May 2025.

27. OECD/G20 Inclusive Framework on BEPS, Statement on a Two-Pillar Solution, October 2021.

28. Institute for Fiscal Studies, Council Tax and Residential Property, 2019.

29. Zucman, G20 Report, 2024 (see reference 8).

30. Ibid.

31. Survation poll for Patriotic Millionaires UK, June 2025; Zucman, Berkeley lecture, 2025.

32. OpenSecrets.org, Top Individual Contributors: All Federal Contributions, 2020 cycle.

33. Electoral Commission, UK political donations register, 2001-2020, compiled by Transparency International UK.

34. Julia Cage, The Price of Democracy, Harvard University Press, 2020.

35. OpenSecrets.org, Lobbying: Top Industries, 2023.

36. BBC Panorama, ‘The Lex Greensill Story’, August 2021; figures subsequently widely reported by FT, Reuters, ITV and SCMP.

37. Finance Act 2003, section 116(7) (treating bulk purchases of six or more dwellings as non-residential); HMRC, Stamp Duty Land Tax: Higher Rates for Additional Dwellings, 2016.

38. HMRC Inheritance Tax Statistics, Table 12.10; IFS, Inheritance Tax, 2021.

39. Green Party of England and Wales, 2024 General Election Manifesto: Real Hope, Real Change — Creating a Fairer, Greener Economy, June 2024.

40. Wes Streeting MP, wealth tax proposal (capital gains tax equalisation), as reported in national press, 2026; revenue estimate by the Centre for the Analysis of Taxation (CenTax)